Dollar-Cost Averaging (DCA)

Dollar cost averaging sounds technical, but as far as investment strategies go, it’s one of the simpler ones. It can be a good way to think about how you might want to approach investing, especially if you’re new to it. You might not be aware of it, but if you’ve got a KiwiSaver account, you’re probably already doing it.

What is dollar-cost averaging?

Firstly, dollar cost averaging involves choosing an investment option that suits you. Then, investing a set amount of money into it regularly over a period of time. This is done regardless of the price or market conditions, meaning you don’t have to worry about trying to time the market to get the best price.

The market tends to trend upward over the long term, as evidenced by historical performance. By using a dollar cost averaging approach to investing, you’ll hopefully end up with more units or shares than you might have if you’d saved up a lump sum over a longer term to make a one-off investment later.

However, it’s important to know that no investment strategy can guarantee positive returns. No one can predict how the price of units, shares or other investments are going to change over time, so there is always risk when it comes to any investment.

How dollar-cost averaging works

We’re sure you’ve heard this a million times before, but the basics of making money from your investments is to buy low and sell high. But how do you know what a ‘low’ or ‘high’ price is? If you invest $1,000 into a managed fund when unit prices are $5, then see they’ve dropped down to $4 the next day, you might feel a little silly. Where your $1000 bought you 200 units, if you’d just waited another day your $1000 would have bought you 250.

Let’s say you invested $100 every month into a managed fund over the next ten months instead. Each time you invest $100 you will buy units at the price at the relevant time. Of course, this means some months you’ll buy less units when prices are higher but on the other hand buy more units when prices are lower. By doing so, a lot of the emotion gets removed from the equation. It also helps make investing part of your everyday life, especially if you set it up to work automatically.

Dollar-cost averaging in action

Let’s take a look at dollar cost averaging in action with our hypothetical investors Jane and Mike.

After a bit of research, both Jane and Mike have found a managed fund they believe to suit their circumstances, and each want to invest $1000 into it.

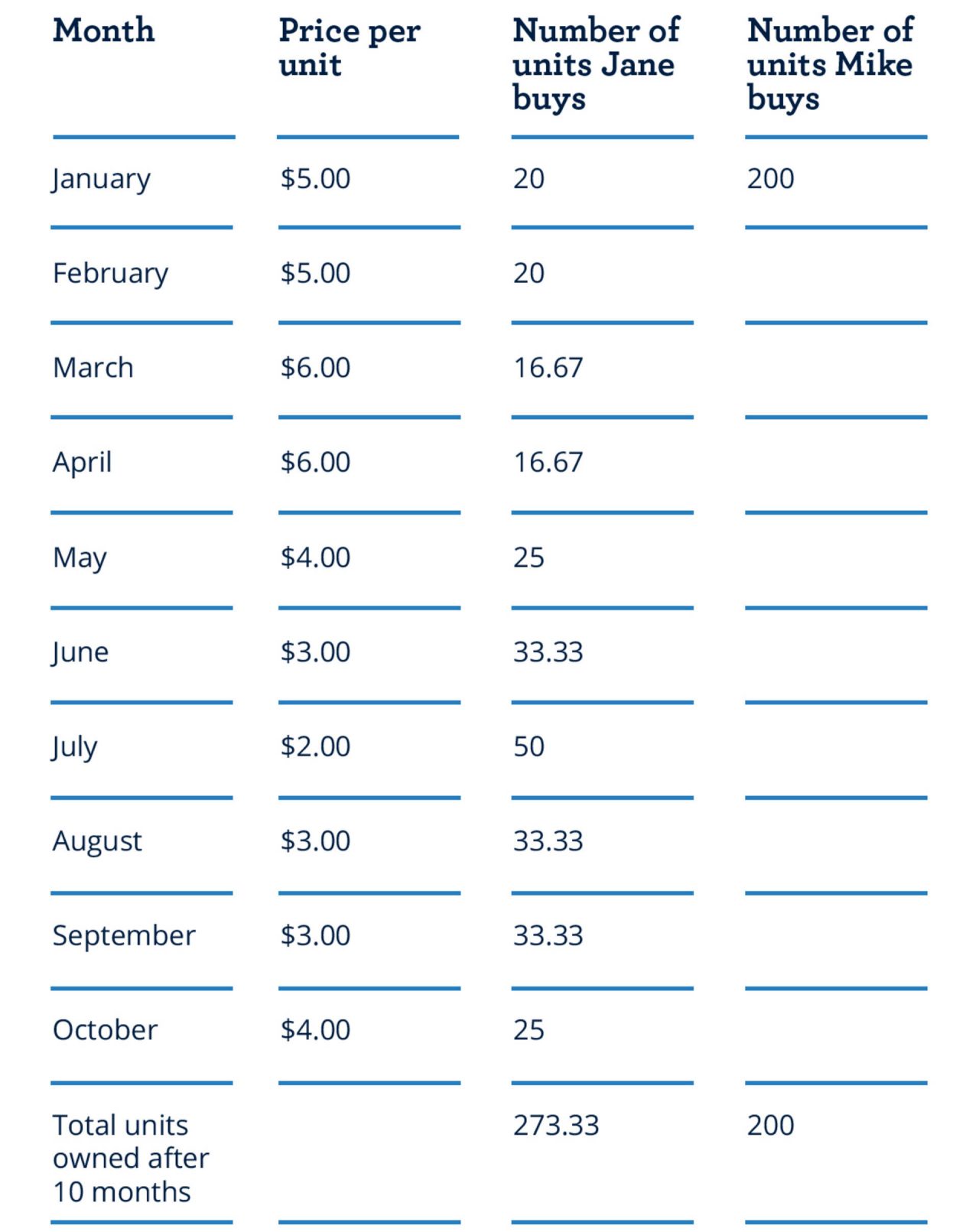

Mike looked at how this managed fund had performed over the last year and saw that its unit price was generally between $5 and $6. He noticed that the unit price climbed in December to $7 and was dropping again. He decides to invest in the managed fund at $5 a unit in January. Mike invests his $1000 which gets him 200 units.

Jane recently read about dollar cost averaging, so she decides to give this approach a go. She decides to invest $100 each month for the next 10 months, regardless of how the managed fund is performing. In January, Jane invests $100 and gets 20 units. Over the next month, the managed fund unit price drops to $4, so she invests another $100 in exchange for 25 units.

As the market fluctuates over the year, Mike keeps tabs on how the managed fund is performing while Jane continues to invest regardless. Let’s look at how their investments went over the next 10 months.

At the end of October Jane has 273.33 units in the managed fund whereas Mike only has 200 units. The value of these units at the start of November is $4, which means Mike’s initial $1000 investment is now worth around $800. Some of Jane's units were bought at a higher average cost than Mike, and some were bought at a lower average cost. Jane’s same investment of $1000, invested using a dollar-cost averaging approach over the same period, is now worth $1,093.32.

The market ups and downs across the year means that (as of the start of October) the value of Mike's units is less than he started with while Jane’s is worth more. Both Mike and Jane have heard that markets tend to trend upwards over the long term, so they both hold onto their units until their value gets back up to $6 three years or so later.

If they choose to sell their units then, Mike would end up with around $1200 from his initial investment of $1,000, whereas Jane's would now be worth around $1,640. Even though they had the same amount of money to invest, and they started at the same time, Jane would make investment gains of around $640 – whereas Mike would only make $200 in gains.

What are the risks of dollar-cost averaging?

Jane and Mike’s investment story is one example of how dollar-cost averaging can work out in the long run but it's important to note that dollar cost averaging doesn't guarantee profits or protect against losses.

While a dollar cost averaging approach can work when the market is falling or remaining relatively flat, it may not be the best approach if the market is lifting while you invest. If the market is lifting, your expected return from a lump sum investment made early on may work out to be higher than investing bit by bit.

If you're looking to invest a little bit at a time or are concerned about investing a lump sum at the wrong time, dollar cost averaging could be an investment strategy you want to consider.

When you invest with AMP, we make it easy to invest what you can, when works for you. Set up a regular payment weekly, fortnightly, 4-weekly or monthly with no minimum investment. Not an AMP member yet? Start investing with AMP today.

Need help with investing?

Knowing where to start with investing can be challenging. Because everyone's needs are different – there's no one size fits all. At AMP, we offer a range of investment options that may suit you. It’s a good idea to seek financial advice or other professional advice relevant to your personal financial situation. We recommend you contact your Adviser, or, if you don’t have an Adviser, contact us on 0800 267 5494.

Recommended reads

Guide to auto-investing

Put your investing on repeat. Learn about auto-investing - the consistent investment approach to help save for your future. Learn more >

Guide to index investing

Explore what index investing is and why it can be a smart strategy for Kiwis looking to enter the investment game. Learn more >

Managed Funds, KiwiSaver, or term deposits?

Explore the key differences between Managed Funds, KiwiSaver and term deposits. Learn more >

This article doesn't provide financial advice on your investment choices. Any information we provide is general only and current at the time. You should consider seeking advice when considering whether an investment is appropriate for your objectives, financial situation or needs.