You deserve outstanding value

We’re proud our AMP Balance Fund No. 2 has been awarded the Canstar 5-star rating for Outstanding Value.

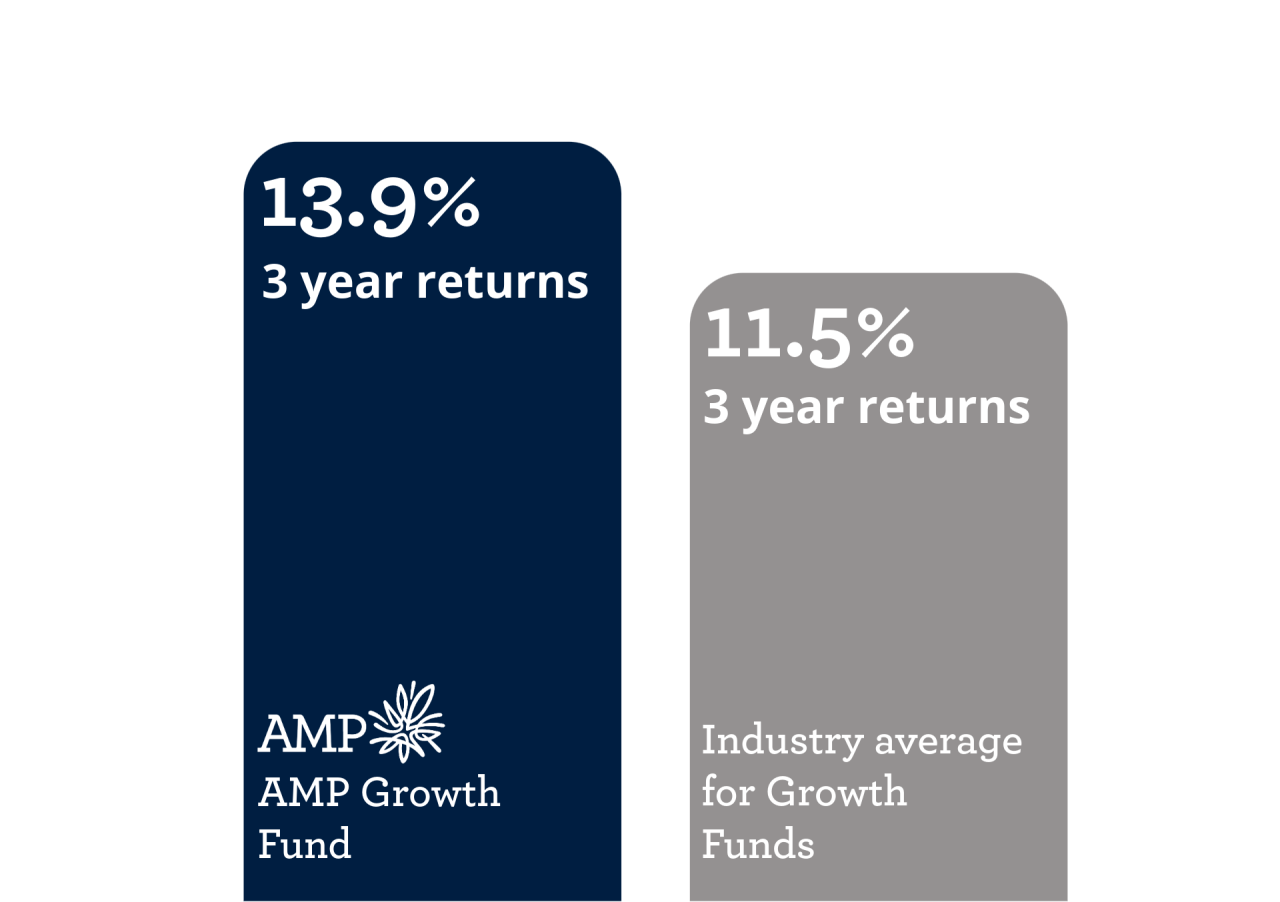

Source: Morningstar monthly KiwiSaver Survey*

Strong returns + low fees

Our AMP Growth Fund has delivered 13.9% in 3-year returns as at 30 November 2025, consistently beating the average investment returns for KiwiSaver funds in the same category across 1, 3, and 5-year returns, a strong result since we changed our investment approach. What's more, our fees are low and we don't charge extra performance fees for strong returns.

This means you get strong returns and lower costs without sacrificing your commitment to sustainability.

View our KiwiSaver performance here

Take control of your savings with help from an expert

Expert guidance can boost your KiwiSaver returns by hundreds of thousands of dollars**. How? A financial adviser will make sure you are in the right fund and are investing just right for you by coming up with a personalised plan for your age and stage of life.

Learn more

Webinar: A year in review & what's ahead

Watch the replay and gain insights into market trends and what they could mean for your financial future. Hear from Aaron Klee, AMP, and Ben Powell, BlackRock, as they wrap up the year and look ahead to 2026.

Watch here

* Source: Morningstar monthly KiwiSaver Report as at 30 November 2025. All returns shown are before tax and after fees (except any membership fees charged in dollars, AMP charges $23.40p.a.). Past performance is not indicative of future performance. Investing involves risk. No person or entity guarantees the performance or any investment of the AMP KiwiSaver Scheme, AMP Managed Funds, or New Zealand Retirement Trust (“NZRT”), including the returns on that investment. The minimum suggested investment timeframe for the AMP KiwiSaver Scheme Growth Fund is more than 3 years.

** Research Source: FSC - Money & You - August 2020.

AMP KiwiSaver Data Sources: AMP KiwiSaver Scheme Annual Report for the year ended 31 March 2025. Our strong results are a reflection of many things, including how we invest your money. We focus on providing simple, low-cost index funds designed to deliver consistent, long-term returns regardless of short-term ups and downs. We appreciate the trust you place in us as your investment provider, and with over $11 billion under management, it’s a responsibility we take seriously. Our Financial Advice Provider Disclosure Statement is available at amp.co.nz/advice-disclosure.